How Finance Drives Monopoly Power

Part 3: The finance-monopoly freight train

Welcome to The Counterbalance, the newsletter of the Balanced Economy Project.

** This post has been updated and slightly expanded since the original publication **

How Finance Drives Monopoly Power

Britain is embarking on a reckless spree of post-Brexit financial deregulation, with eerie echoes of what preceded the global financial crisis of 2007/08. As a top UK regulator put it recently, we tried this before and “it didn’t end well, for anyone.”

The “Edinburgh Reforms” announced last week will undo many safety systems put in place after the great crisis that emerged 15 years ago. Related draft legislation is currently moving through parliament which will, among other things, turn financial regulators into cheerleaders for the financial sector, by forcing them to care about “competitiveness” - a recipe for a race to the bottom between jurisdictions on who can lower their standards the fastest.

A train of top regulators and former regulators and finance experts has come out recently against these sugar-rush reforms (see here, here, here, here, here, here, here, or here, just for instance) and in May we signed a letter, co-signed by some of the world’s most prominent economists, laying out how foolish, incoherent and dangerous the broad “competitiveness” agenda is. Civil society actors have recently added their voices. Here is one, with a spicy but accurate headline.

Among other things, the reforms will increase monopoly power (a term we use broadly, to mean excessive and sustained concentration of market power.)

The Balanced Economy Project, in partnership with the finance experts Gerald Epstein (University of Massachusetts Amherst) and Andrew Baker (Sheffield University,) has just sent a detailed submission to the Bank of England, in part explaining how “competitiveness” in finance harms competition, and showing how best to minimise the damage if the politicians force the “competitiveness” objective onto them.

Curbing financial sector excesses will have profound effects on curbing monopoly power. This article follows our earlier publication “How Finance Drives Monopoly, Part I” (which focused on private equity). Now we broaden out the connections, with a brief shortlist of some ways in which finance drives monopoly power.

1. "Deals" and Dealmaking

“Dealmakers” in the Mergers & Acquisitions (M&A) departments of large investment banks earn enormous fees for assembling M&As. Crucially, they are not just passive facilitators, but active drivers, often initiating and encouraging harmful mergers and mega-mergers. One M&A focused website notes, for instance:

Here’s a list of the top banks advising on M&A this year:

Journalists often report on this “dealmaking,” unquestioning, even in heroic terms. In doing so they are, to a significant degree, cheerleading harmful monopolisation.

2. Kill zones, predatory pricing

Finance likes to throw cheap, plentiful credit at powerful, wealthy monopolists like Amazon, while starving their competitors. Venture capitalists talk of “kill zones” where innovative firms can’t access reasonable financing because lenders judge them to be operating in areas where the monopolists can kill them at will.

Monopolists often use their preferential access to cheap finance to pay for predatory pricing strategies. As Matt Stoller put it:

“The goal . . . is to find big markets and then dump capital into one player in such a market who can underprice until he becomes the dominant remaining actor. In this manner, financiers can help kill all competition, with the idea of profiting later on via the surviving monopoly.”

Finance can confer competitive advantages even when deliberate predatory pricing isn’t involved. Our forensic analysis of children’s social care in the UK, and our detailed submission to the UK’s Competition and Markets Authority (CMA,) showed how superior access to finance allowed private equity and other large firms to out-compete smaller and often more accountable care providers, on factors that had nothing to do with superior quality of service, and everything to do with having better access to finance, and greater willingness to use debt to juice up returns.

This access to finance will tend to tip markets towards monopoly, including through a “competitive contagion” where other firms feel the need to adopt similarly damaging finance-heavy strategies, if they are to stay in the game.

3. Roll-ups

Private Equity firms commonly buy up many different firms in a market niche, like funeral homes, dentistry, or social care - often with a narrow geographical focus. They may roll up several competitors into a single structure of ownership and control, creating monopoly power in that niche. As top US antitrust official Jonathan Kanter said: “many of the mergers we’re confronting are as a result of [private equity] roll ups.” (We wrote about all that, here.)

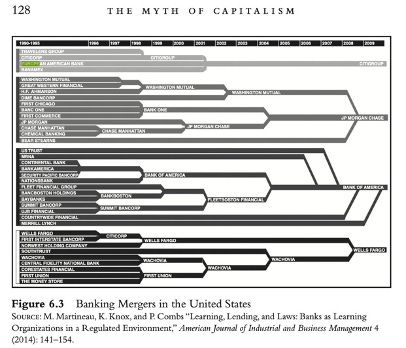

4. Too Big To Fail Banking

Finance has also become an intensely monopolised sector, in its own right. Here are two illustration of this trend: one from the UK, the other from the US.

(Source: PwC; and The Myth of Capitalism, Jonathan Tepper and Denise Hearn, 2020.)

Banks, of course, are just one part of any financial sector. This is a large and complex subject, which we will return to, another day.

5. Finance cartels and other arrangements

Cartel-like behaviour is common in finance. The best-known are probably the Libor cartel, interest rate derivatives cartels, the bond trading cartel, the forex trading cartel, and so on.

The U.S. term “antitrust” goes back to a similar but different game: the great “money trusts” of interlocking financial power that allowed a small group of financiers to lock up large parts of the U.S. economy, until people power broke them apart.

A similar but different kind of arrangement in the modern day exists via large global asset managers like Blackrock, State Street and Vanguard. Investing on behalf of millions of people, their Exchange Traded Funds and other vehicles hold stakes across an enormous swathe of our economic landscape: especially in large listed firms with market power. These 'concentrated financial ownership' patterns may grant the managers of firms significant control over their management, which may further spur monopolisation.

6. The Big Tech - Finance merger

There is a large and fast-developing alliance and interdependence between monopolising Big Tech firms and finance, in what has been called “the Financialisation of Big Tech”. The latest example may be Microsoft’s decision to buy a four percent stake in the London Stock Exchange, to work together on cloud tech and data analytics. Brett Scott’s 2022 book Cloudmoney begins thus:

A report by Finance Innovation Lab. in the UK, also looks through the hype of "fintech" and notes three key trends: first, Big Tech becoming a financial services provider; second, Fintechs, banks, and other financial services firms developing and learning from the platform model; and third, Finance becoming ever more reliant on critical digital economy infrastructure controlled by Big Tech.

Big Tech will be far more easily able to subjugate Big Finance in the long term, than the other way around.

7. Offshore finance, monopoly power and data havens

Another, messier nexus exists between finance and competition, via the world of secretive offshore tax and financial havens, and the race-to-the-bottom “competitiveness agenda” we mentioned above.

A new term is now emerging: data havens. Companies have often chosen to locate their data operations in countries where the rules and enforcement are most lax, usually in small countries where it is relatively easy to 'capture' or influence legislators and enforcers. Favoured places are also, not by coincidence, notorious corporate tax havens, such as Ireland and Luxembourg.

8. The market for corporate control

This one ties several of the last sections together. Milton Friedman had famously argued that corporations should be run for the benefit only of shareholders - and not for other stakeholders such as workers, communities, taxpayers, the broader economy, or other purposes. We’ve often mentioned another Chicago-School thinker, Robert Bork, who argued that regulators should stop worrying about those other stakeholders, and instead focus on the interests of consumers. But there is a third Chicago-School thinker, Michael Jensen, who put Friedman’s ideas on steroids, in a new finance ideology.

Jensen argued that the interests of corporate bosses weren’t sufficiently aligned with those of stockholders, so three further steps were needed. First, tie executive pay to stock prices, with stock options and so on, to make them focus more laser-like on stockholders. Second, increase executives’ share-price anxiety by loading companies up with debt, to juice returns even further.

Then, as Counterbalance author Nicholas Shaxson wrote in the Literary Hub:

“The third, grandest prescription was to relax laws to allow for the development of a full-blooded “market for corporate control,” where financial players would buy and sell companies across the global economy as if they were cartons of orange juice. The free market, thus unleashed from above onto the corporate landscape, would magically dismantle and rearrange the corporate world in a blur of dealmaking to deliver a great surge of efficiency to the economy.”

Reagan-era deregulation ushered in a flood of dealmaking, and this global “market for corporate control” put financial players in positions of rising power over the corporate (and political) landscape - a position that they remain in, today.

Endnotes

We’re hiring!

Please see our recent job posts, for an exciting international network co-ordinator role for anti-monopoly work, and an administration/operations role. We will likely have more part-time and even full time roles coming available in due course: please consider getting in touch. (Please also see this newly advertised role for an EU Advocacy Officer, from our allies at Article 19.)

How Musicians Get Paid - Balanced Economy Project

“On one occasion, I counted 50 million views of a video for a song I’d written on Youtube, and I got paid £158 for that, over three years. I made more money busking in an afternoon in Bath.” Musicians suffer under several lawyers of monopoly power. Including the Ticketmaster/Taylor Swift row.

We’re taking on Amazon’s billion-dollar takeover of iRobot - Foxglove

A letter to the UK’s CMA to say: enough is enough. This is a buy-out too far: the Amazon / iRobot deal needs investigating, and probably should be blocked.

Data anarchy at Meta - Irish Council for Civil Liberties

The ICCL has sent a letter to the European Commission highlighting shocking new material about Meta’s internal data systems. This, ICCL argues, seems to meet the test of systematic non-compliance with the Digital Markets Act (DMA): the Commission should impose "structural remedies" - break Meta up. See also this shocking exposé by ICCL and partners on the advertising free-for-all known as “Real Time Bidding.”

Who killed the vaccine waiver?

In the past, the United States has protected monpoly power for its multinationals, especially via the TRIPS system. This time, the Europeans have been the main culprits. (See also our recent article, The quadruple tax system of patent monopolies.)

The hidden trend reshaping and hurting the Canadian economy: serial acquisitions

Denise Hearn, Robin Shaban. Alongside the mega-mergers, “creeping acquisitions” are now endemic to Canadian life. They fall in a competition policy blackhole, are little-noticed, and are a favourite of private equity firms.

The effects of mergers: more evidence against the ‘efficiency defence.

Profits go down, workers earn less. A new paper by David Arnold, Kevin Milligan, Terry Moon, and Amirhossein Tavakoli on post-merger firm performance, which "raise doubts on the efficiency arguments made in support of M&As."(Again, in a Canadian context.)

More on corporate power and the drivers of inflation

This article in Social Europe looks at how monopolisation in commodity supply chains, and market power enjoyed by financial intermediaries, has been helping drive inflation. (See also ETC Group’s “Food Barons 2022” update on consolidation in agriculture and food, from September.

A new report from the Roosevelt Institute shows markups (basically, how far prices are above costs) rising from an average 26 percent in 1960-1980 to 72 percent in 2021. “Moreover, 81 percent of the average increase in markups from 1980 to 2019 came from increases within industries, pointing to a generalized increase in market power.”

European State Aid control fails to get traction in tax deal

The European Court of Justice has, in a final decision, quashed a decision by the Commission that Fiat's special tax deal with Luxembourg was illegal State aid. This decisions essentially rules that State aid control should stay away from company tax deals. Another judgement, with Apple, is pending, but the Commission now looks even more unlikely to win it. Poorer individuals and smaller businesses will have to pay the taxes that multinationals won't.

Breaking up HSBC

Calls for the global breakup of HSBC. "the financial embodiment of globalisation", are coming from inside the bank, reflecting intense geopolitical stresses.

Push to give teeth to UK's Digital Markets Unit

A new report by UK Members of Parliament urges the Government to publish a draft Digital Markets Bill that would help deter predatory practices by Big Tech firms ‘without delay’. The current legislative framework for the UK's competition regime dates from 1998 and 2002. The UK has led the world in some areas. Now, at last they are taking the DMU seriously, and moving fast. See also Full Steam Ahead for the Digital Markets Unit.

Do Competition Lawyers Harm Welfare?

This article by Richard Whish complements our widely read interview with Tommaso Valletti, who saw, and rejected, a corrupt worldview in the competition establishment. Among various other things, Whish raises the point that common legal efforts to hamstring regulators with endless delaying tactics could be tackled with "interim measures," flipping the incentives. See also Jan Broulík's recent article on the cultural capture of antitrust.

India forces Google to allow third-party payments

App developers will no longer have to use Google's payment system for user transactions there.

Democracy’s Library

The Internet Archive has begun collecting the world’s government publications into a single, permanent, searchable online repository, so everyone—journalists, authors, academics, interested citizens—will always be able to find, read, and use them.

From the U.S.

Integrating competition with data protection

The U.S. FTC is looking to integrate data protection more closely into merger reviews. Current approach of “We do market power over here, data protection over there” isn't working. Integration makes sense, everywhere.

Making platforms (more) responsible for content?

Gonzales et al. vs Google, from the family of a victim killed by ISIS terrorism, addresses a free speech conundrum. Some argue for repeal of U.S. rules ("Section 230") that absolve platforms of responsibility for e.g. violent content. Free speech advocates say this goes too far (and is illegal): a bit like making phone companies responsible for what people say on phone calls. This case seeks a middle way: don't make the platforms responsible for the content itself, but seek ways to make them more responsible for algorithms that promote it. Update: See also Twitter v. Taamneh; and also “Son sues Meta over father's killing in Ethiopia,” (involving Foxglove again.)

New wins for reinvigorated U.S. antitrust enforcers

Alongside the private equity victory, we see that the US Department of Justice Antitrust Division recently won its first Section 2 criminal monopolisation case in 50 years. The U.S. DoJ also announced that some companies are unwinding 'interlocking directorates,' amid beefed-up enforcement. See also "Antitrust Enforcement is Back", on the blocking of Penguin Random House's takeover of Simon & Schuster. See also Matt Stoller's recent piece on a U.S. antitrust judge blocking a large dividend recapitalisation - a common form of Private Equity looting. (See also "Ten Tricks: a short handbook of financial engineering," by the global union Public Services International, with our help.)

The Law of Networks, Platforms, and Utilities - UPenn

In recent decades, public utilities laws and “the law of common carriers”— has died as an integrated field of study, replaced by a bipartisan distrust of public administration and a faith in the self-regulating power of markets. This new casebook entitled Networks, Platforms, and Utilities: Law and Policy seeks to revive the field.